Author: World Bank Group

Site of publication: World Bank

Type of publication: Report

Date of publication: 2025

Notes

The State of the Economy

Guinea-Bissau faces several important structural challenges to improve growth prospects including reoccurring political instability. A poor national road network, a low-production seaport, and costly access to the internet hamper efficient access to markets and the development of national and regional value chains. A challenging business environment, paired with policy uncertainty and weak institutions, undermine private sector investment, preventing progress in economic diversification.

The economy remains highly dependent on the export of raw cashew nuts. These make up around 90 percent of export value and provide income to around 80 percent of the population, mainly smallholder farmers and temporary harvest workers. Only around 3 percent of domestic output of raw cashew nuts is processed locally into eatable cashew nut kernels.

Guinea-Bissau lacks a conducive enabling environment for private sector-led growth due to low levels of infrastructure, human capital, and public services. This situation is compounded by strong elite competition for rents and a weak public administration.

Recent developments – Real sector

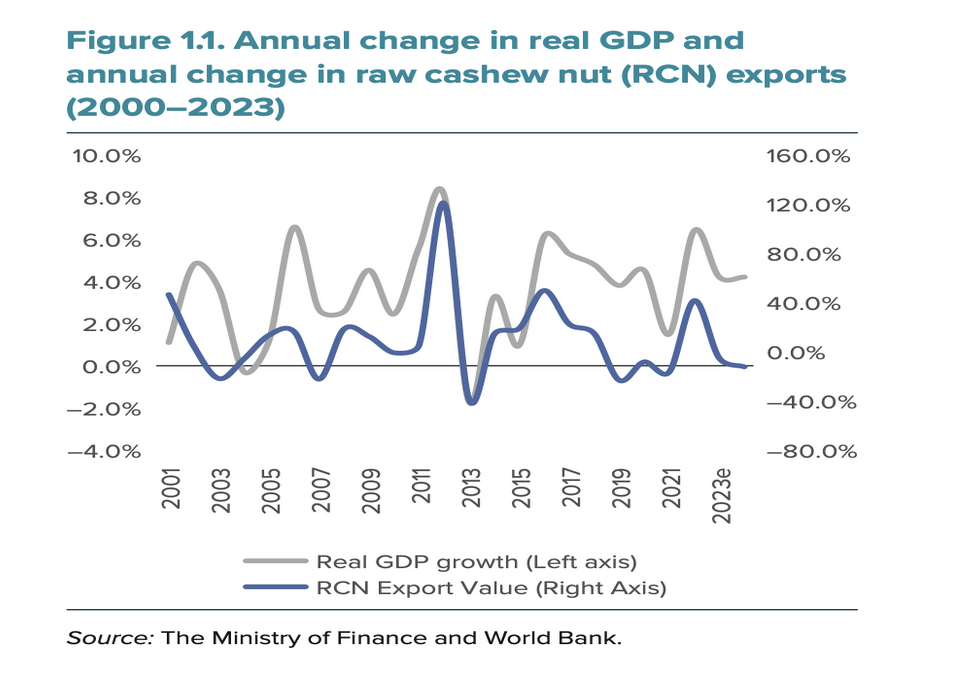

Growth remained unchanged at 4.2 percent in 2023 as challenges in export performance limited the translation of record-high cashew production into growth. Headline inflation remained high at 7.2 percent, with rising food prices prompting the authorities to introduce price controls and subsidies on key goods.

The economy remains highly dependent on the export of raw cashew nuts. These make up around 90 percent of export value and provide income to around 80 percent of the population, mainly smallholder farmers and temporary harvest workers. Only around 3 percent of domestic output of raw cashew nuts is processed locally into eatable cashew nut kernels

Guinea-Bissau’s cashew campaign was not disrupted by the 2023 legislative elections as much as anticipated, but weak international demand and high levels of smuggling kept economic growth below potential at 4.2 percent. A difficult cashew campaign limited the translation of high production into economic growth. While cashew production reached 260 thousand tons, the highest production yield on record, only 170 thousand tons were exported by the end of 2023.

Fiscal and debt dynamics

Fiscal consolidation efforts were derailed as higher- than-planned discretionary spending and lower customs receipts widened the fiscal deficit to 7.6 percent of GDP in 2023.

The fiscal situation worsened in 2023. Despite the government’s commitment to a fiscal consolidation program that preserves medium-term sustainability, the overall fiscal deficit widened to 7.6 percent of GDP in 2023, from 6.1 percent in 2022 (on a commitment basis). This reflects poor revenue performance and higher-than- expected discretionary spending, which have also contributed to the widening of the primary balance (from 4.7 percent of GDP to 5 percent in 2023). While ongoing fiscal consolidation efforts have crowded in grant commitments, not all have materialized.

Total revenues fell in 2023, driven in part by a fall in tax revenue. Total revenues fell from 15.2 percent of GDP in 2022, to 13.9 percent in 2023 driven by poor export volumes of cashew, the introduction of rice subsidies financed by exempting the private sector of import tax duties to set the price of rice below market value, and lower grant Financing.

While expenditures remained largely unchanged as a share of GDP, this masks the significant increase in discretionary spending and rising interest payments. Despite this slippage, steady progress is being made to strengthen domestic revenue mobilization, rationalize the wage bill, and improve overall expenditure control

The authorities remain committed to implementing measures to strengthen domestic revenue mobiliza- tion (DRM) with notable steps taken in 2023.

Public debt remains above the WAEMU convergence criteria, and fiscal risks – particularly from SOEs – persist.

Total revenues fell in 2023, driven in part by a fall in tax revenue. Total revenues fell from 15.2 percent of GDP in 2022, to 13.9 percent in 2023 driven by poor export volumes of cashew, the introduction of rice subsidies financed by exempting the private sector of import tax duties to set the price of rice below market value, and lower grant Financing

Public debt remained relatively high, at an estimated 77.8 percent of GDP, in 2023 despite falling from 80.4 percent in 2022 – with external debt accounting for a smaller share. The decline in the ratio is largely attributed to higher nominal GDP growth, as nominal debt levels continue to rise. This increase was driven by a higher-than-planned fiscal deficit.

Balance of payments

High food and energy import costs maintained the CAD at the same level as in 2022 but the IMF SDRs were increased by 140 percent to continue support financing needs

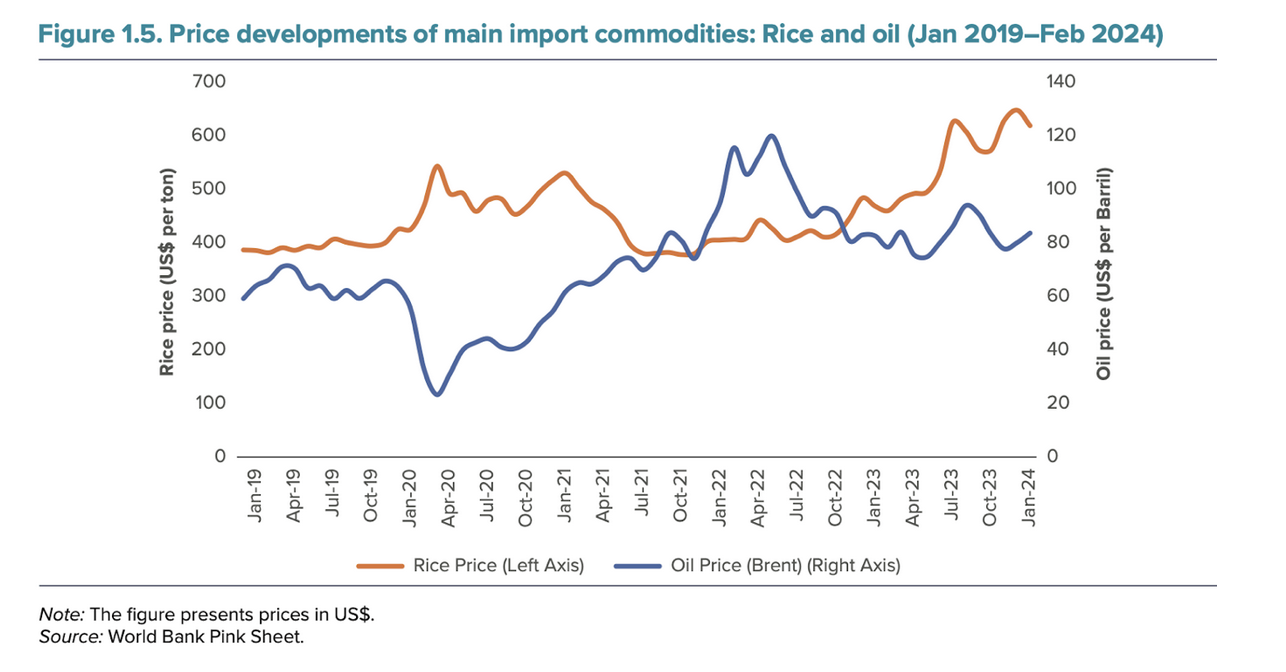

The current account deficit (CAD) remained broadly unchanged from 2022, driven by the high costs of food and energy imports. The country is highly dependent on imports for most sectors, such as staple foods, fuel, medication and building materials.11 Inflationary pressure on essential goods and services (Figure 1.5) that Guinea-Bissau imports eased in the second half of the year supporting a slight improvement of the CAD despite poor cashew export performance. Consequently, the CAD fell from 9.6 percent in 2022 to 9.4 percent in 2023.

Monetary policy and the financial sector

The stock of credit to the private sector remains below the WAEMU average and credit to the economy grew but decelerated in 2023. The banking sector remains fragile.

Inflationary pressures began to ease in the second half of 2023, possibly supported by price controls on staple foods that were driving inflation. Inflationary pressure increased after the pandemic driven by supply chain disruptions and a global increase in commodity prices caused.

Despite appreciating in recent years, the real effective exchange rate (REER) remains around 2010 levels. The CFA peg to the euro has kept the REER relatively stable since 2010. REER changes tend to follow the nominal effective exchange rate (NEER), as the inflationary differential with trading partners is minimal. The REER has appreciated about 4 percent since 2019 but remains around 2010 levels. Shallow financial markets limit financial inclusion and development.

Access and use of financial services have increased in the last decade, fostered by the government’s decision to pay salaries only through the banking sector, but it remains low. Recent data in this area is difficult to obtain in Guinea-Bissau but the stock of credit to the private sector was approximately 15 percent of GDP end- 2021, below the WAEMU average of 22 percent of GDP. Increasing the use of mobile phone services could advance financial inclusion by giving people outside of Bissau access to financial services. The liquidity of the banking system was supported by the accommodative stance of the BCEAO, and credit to the economy grew but decelerated in 2023.

Poverty

Poverty has followed an upward trend in Guinea- Bissau since 2018 and is more pronounced in rural areas than urban areas because of low productivity agricultural production.

Poverty continues to be widespread in Guinea Bissau- increasing by 2.8 percentage points (equivalent to over 80,000 additional poor) between 2018 and 2021.

This is partly because the rural economy continues to be dominated by low-productive agriculture – mainly raw cashew nut production. Over 70 percent of house- holds rely on cashew production in Guinea-Bissau, for whom income from the sale of cashew nuts is an important source of livelihood.

The rural-urban disparities in well-being may also have been further exacerbated by the faster post-COVID-19 recovery of the services sector – which employs most of the urban households. For instance, the services sector grew by 7.5 percent in 2021 – from 0.35 in 2020 and 3.2 in 2018; mitigating the adverse effects of the COVID-19 pandemic thereby resulting in a smaller increase in poverty in urban areas relative to rural areas.

More than half (55 percent) of the poor are concentrated in the regions of Oio, Gabu, and Bafata. In addition to having a high incidence of poverty, the regions of Oio and Gabu are home to 23.7 and 17.1 percent of the poor people in Guinea Bissau respectively

Outlook and risks

Early signs indicate that the 2024 cashew campaign promises to be strong, which will support real economic growth of 4.7 percent. Cashew production is expected to be strong again due to favorable weather conditions and as government investments into agricultural inputs over the last few years pay dividends. In contrast to the previous two years, however, exports should markedly improve as nine overland border routes become authorized for exports, curtailing smuggling.

Easing inflationary pressures along with strong demand for cashew will drive growth on the demand side. Following the worldwide trend, inflation is expected to have already peaked and is projected to fall to 4.5 percent in 2024. Inflation stabilized in 2023, as supply disruptions abated, and fuel and energy prices stabilized. Over the mid-term, the country’s membership in the WAEMU economic and monetary zone, which provides a strong nominal anchor with its peg to the euro, and the govern- ment’s commitment to fiscal consolidation will keep inflation contained, converging to an estimated 2 percent by 2026.

Decreased external pressure in 2024 as fuel and food prices stabilize as well as improved cashew exports will cause the CAD to contract to 5.7 as a percent of GDP.

The authorities are committed to fiscal consolidation to ensure medium-term debt sustainability. The fiscal deficit is projected to narrow in 2024 to 4.8 percent of GDP (on a commitment basis), from 7.6 percent.

Public debt is expected to fall to 75.6 percent of GDP in 2024 and meet WAEMU convergence criteria by 2026.

Global commodity market shocks, SOEs, and the banking sector also present potential risks. In addition to risks arising from volatile global food and oil prices, weaker cashew nuts exports and lower-than-expected donor support may impact the outlook. Financial stress in state-owned enterprises, such as EAGB (Box 1.3), and banking sector fragilities could also generate contingent liabilities adding to fiscal pressures.

Public Sector Pension Scheme in Guinea- Bissau

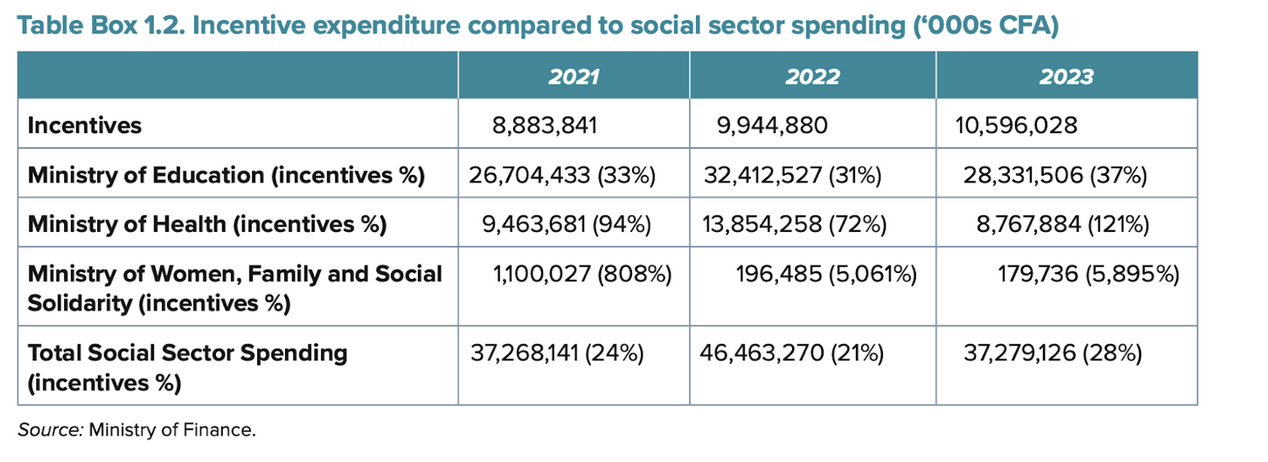

Tight fiscal space and rising debt levels have limited crucial investments in economic and human capital to advance Guinea-Bissau’s economic growth and develop- ment goals.

Analysis and challenges

The 60-year retirement age under the public service pension schemes is in line with international yardsticks. Life expectancy at retirement age determines the length of time during which people collect pensions. The retirement age for the public service pension scheme in Guinea-Bissau is 60 for both men and women while life expectancy at age 60 currently stands at 15.5 years on average. This is in line with the international yardstick of 15 years for the “ideal” duration of pension benefits. As such, the current retirement age of 60 is not particularly low relative to life expectancy.

The public service pension benefit formula leads to generous benefits relative to pre-retirement salary.

Calculating the public service pension based on the average of the last two years of base salary (instead of a longer period) leads to higher pensions. Salaries in the public sector tend to monotonically increase with age. The average salary of civil servants (including military and reserve personnel) who are 58 years of age (158,258CFA) is 27.2 percent above that of civil servants who are 25 years of age (124,463CFA) while the median salary remains broadly unchanged.

Pensioners and expenditures

The three public service pension schemes pay widely different pension amounts. According to the payroll database, the Ministry of Finance paid 7,045 pensioners in June 2023 (Table 2.4). Of the total number of pensioners, 28 percent (1,964 individuals) were regular pensioners, 48 percent were pending pensioners (3,385 individuals), and 24 percent (1,696 individuals) were veterans.

Recommendations for improvement

Governance: the pension rules are not systematically applied. The management of the schemes makes important discretionary changes to individual pension amounts which do not comply with the rules. This finding combined with the fact that pension payments overly benefit a very small fraction of beneficiaries is unsettling. It gives the perception that pension payments are “captured” by those responsible for the implementation of the schemes. Benefits should be secure and non-discriminatory, schemes should be managed in a sound and transparent manner, and for confidence to exist, good governance is essential.

Design: i. The base wage for pension calculation (reference salary) includes only the 2 last years: this is not only costly but inequitable (by design). Including all (valorized) wages (entire career) in the pension’s calculation would be the fair way to do it between people with different patterns of pay over the career and would also avoid distortions to people’s requesting wage increases just before retirement.

The creation of a pension fund is not likely to resolve the governance challenge. It is not clear how the deposit of 6 percent from the payroll of all public employees into a special account (or pension fund) jointly managed by the Ministry of Public Administration and the Ministry of Economy and Finance as stipulated in the 2015 Budget Law would improve the management of the schemes.